Session 5 - The material conditions of ICT

Browsing through a global footprint

To produce the phenomenal quantity of components, devices and digital equipment used today, it is necessary to ensure a constant and globalized flow of materials. This flow links the mining areas to the manufacturing plants, and these plants to recycling and waste facilities, but could it be maintained? How the material demands of the digital sector relate to the general demand? Furthermore, what is the social and environmental cost of extracting these resources?

Current and future demand for minerals

The extraction of metals requires the opening of a mine, either underground or open. Mines are opened because the industry requires more raw materials or projects to do so. Indeed, investors will generally only fund a mining operation if there is demand and profitability. It is therefore demand that drives the production of mineral raw materials: supply adapts to demand. However, increasing construction and new industries have greatly increased demand.

Jubilee Mine - 6,500 tonnes of copper - Credits: Dillon Marsh

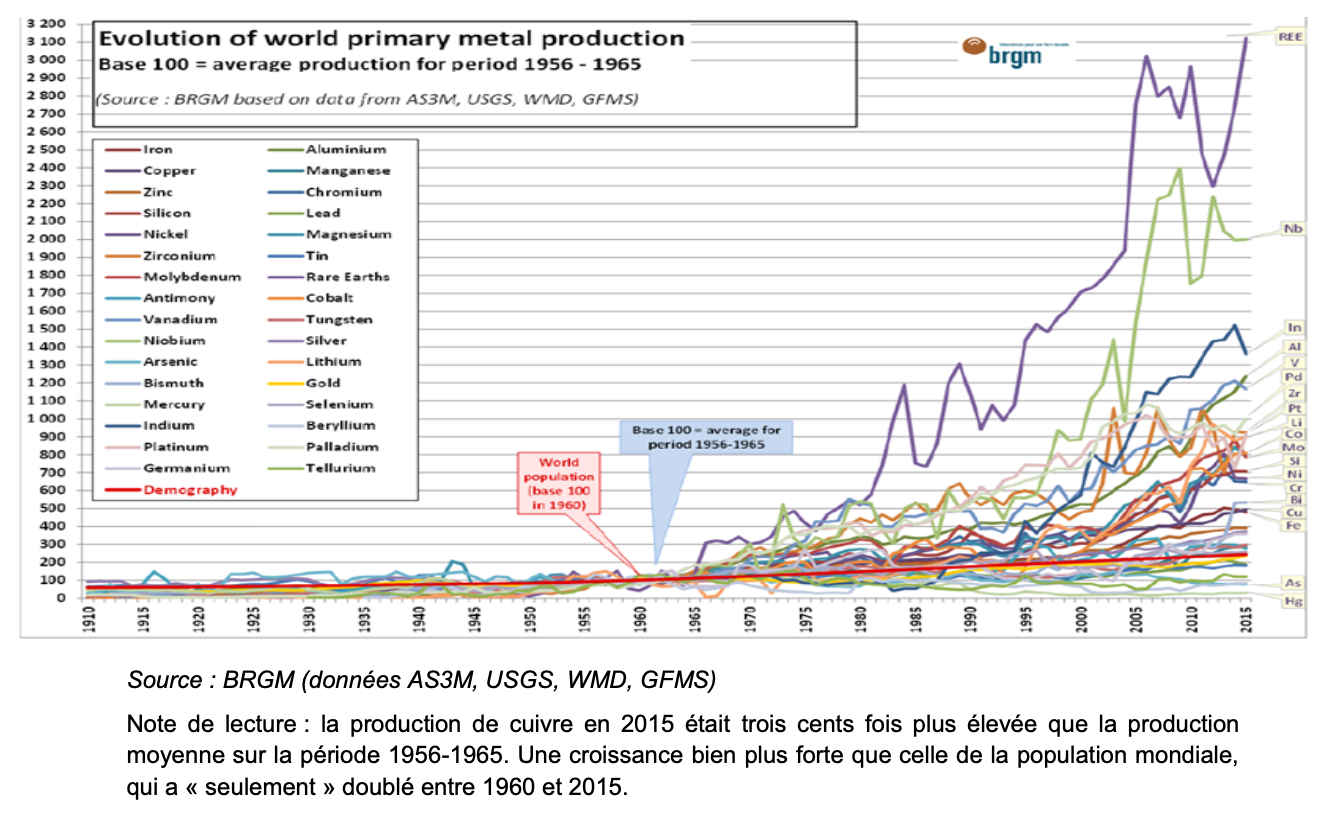

Human societies, mainly industrial, consumed 210 megatons (Mt) of minerals worldwide in 1900, then 6.5 gigatons (Gt), or 6500 megatons, in 2009 . During this period of a little more than a century, the population has multiplied by 4 while the consumption of ores and industrial minerals has multiplied by 30. The latter is mainly due to specific societies and social classes. As such, the 30-fold increase in mineral consumption is not attributable to humanity as a whole, but to certain societies in certain territories over a certain period of time.

Evolution of world primary metal production - Credits: BRGM

Understanding our current reserves

When demand emerges from the industrial and financial sectors, supply does not instantly line up as if it were a matter of releasing stocks. It takes several decades from the beginning of geological exploration, the first drillings, the opening of the mine, to the exploitation and the extraction of the first ton of ore. In the case of exploration in an already known area, this deployment time can be quite "fast", between 10 and 15 years. In the case of an exploration in a little known area, it is necessary to count between 20 and 30 years. It is important to understand that if a demand for a metal emerges in 2020 and investments are released for geological exploration at the same time, then the first tons extracted (supply) to meet this demand will be available between 2030 and 2050. So anticipation is key in the mining sector.

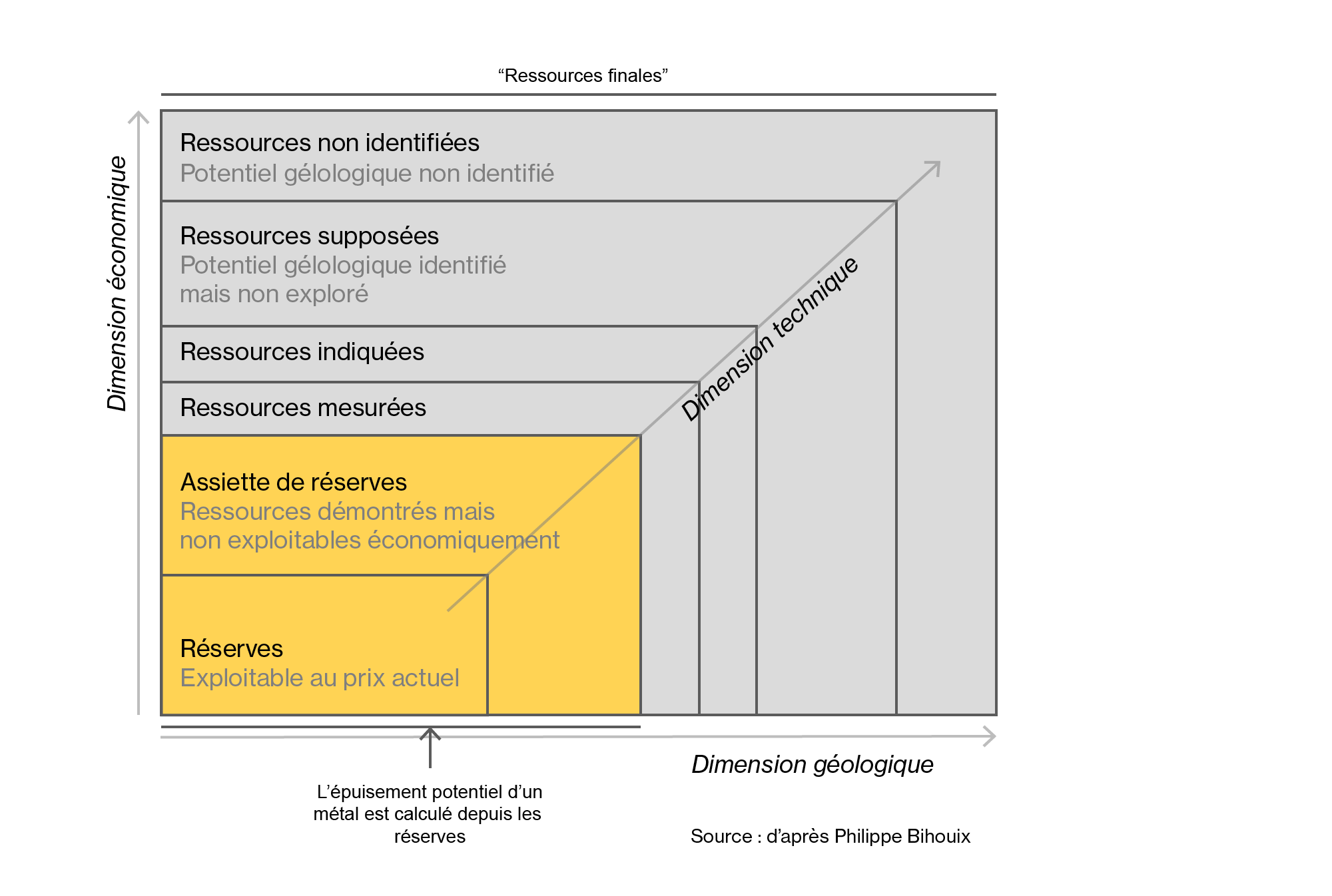

Understanding how to qualify the importance of mineral resources and reserves is not straightforward. There is a clear distinction between two terms: resources on the one hand and reserves on the other. In geology, "resources" correspond to the concentration of a liquid, solid or gaseous substance in the earth's crust. Thus the definition of resources varies greatly according to geological knowledge and the measurement tools available. As exploration and extraction techniques become more sophisticated, the resources discovered or extractable may increase. The more certain we are of an ore concentration in the ground, the more economically qualified the resource is. We then speak of "inferred" resources for the least well identified resources, "indicated" resources and "measured" resources for those that are better known. There are also "unidentified" resources, which are an estimate based on the mathematical probabilities provided by previous explorations.

Reserves correspond to known concentrations of ore that can be economically and technically exploited at a given price at a given time. It is therefore the market price, technological progress in extraction methods and processing costs, geological concentration, quality and depth of the vein that indicate how much of the measured resources become exploitable reserves. There are several types of reserves, two of which are prominent: the reserves base includes all proven resources (measured and indicated) that are mineable by current mining practices. The reserves base includes reserves that are economically recoverable at the time of evaluation (economic reserves), those that are close to being economically recoverable (marginal reserves), and those that are not currently economically recoverable at all (sub-economic reserves). It is from the reserve base that the global reserve of a resource is calculated. The so-called "reserves" are the part of the reserve base that is technically, geologically and economically exploitable at the time of the evaluation. This does not mean that all reserves are exploited, but rather that they could be exploited at the time.

Difference between resources and reserves

The definition of resources and reserves is therefore a complex exercise that depends on geological factors (location, concentration, quality, depth of the deposit), scientific and technological factors (state of knowledge of exploration, drilling, production, design of the necessary machinery), and economic factors (price on the raw material markets, cost of extraction, cost of the energy required for extraction, investment and operating costs). Other factors also come into play, such as the geopolitical factor: resources are not equally distributed in the earth's crust, some countries have "richer" soils than others. There are also social and environmental factors: the opening of a mine and the cost of extraction also depend on the social standards (protection of personnel, salary policy, etc.) and environmental standards (pollution and depollution standards, water use, etc.) of the country where the operation is located. The criticality of a resource, rather than its depletion, is therefore relative to all these criteria.

Future demand

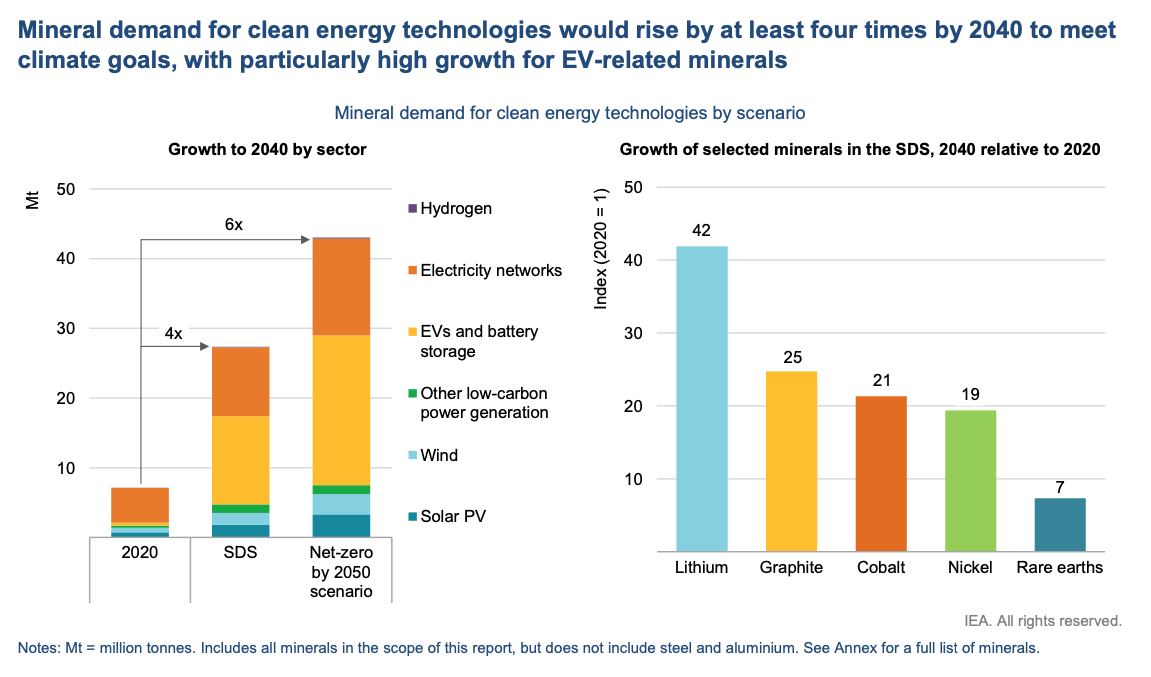

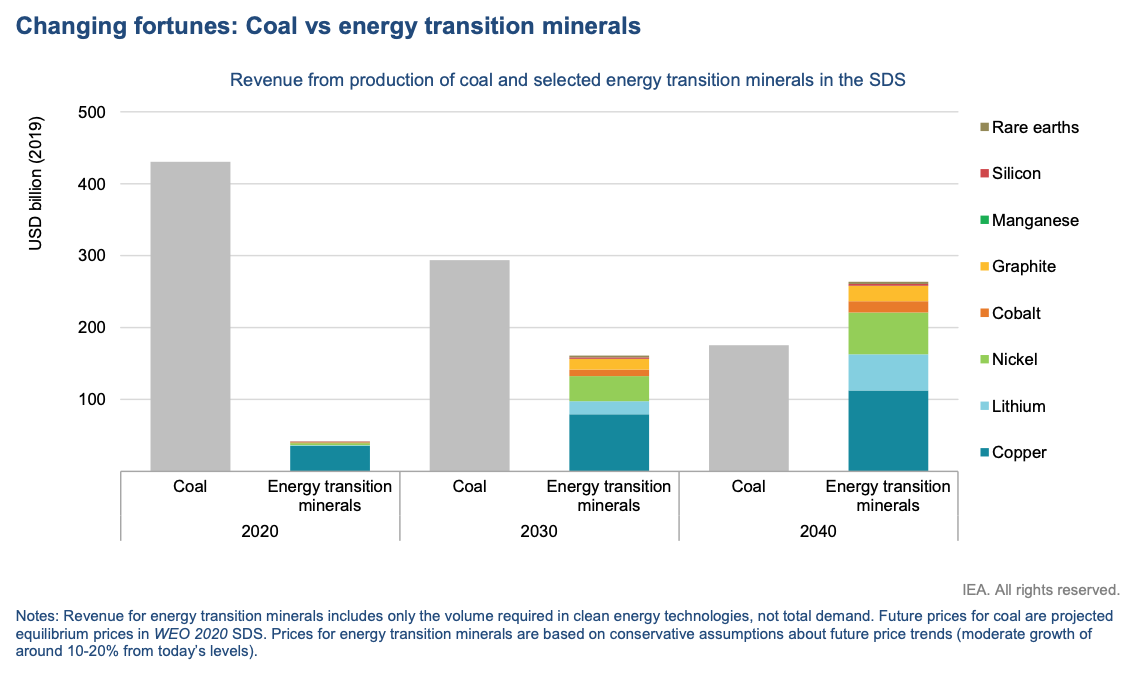

There is a general consensus that global mineral demand is going to increase very rapidly, especially with technologies related to the transition (electric vehicles, renewable energy). In a sustainable development scenario, the IEA estimates that we need to increase our mineral consumption by a factor of 4 between 2020 and 2040. At a time when the most abundant deposits are already being exploited and discoveries of new deposits are slowing down, it seems impossible to meet this demand.

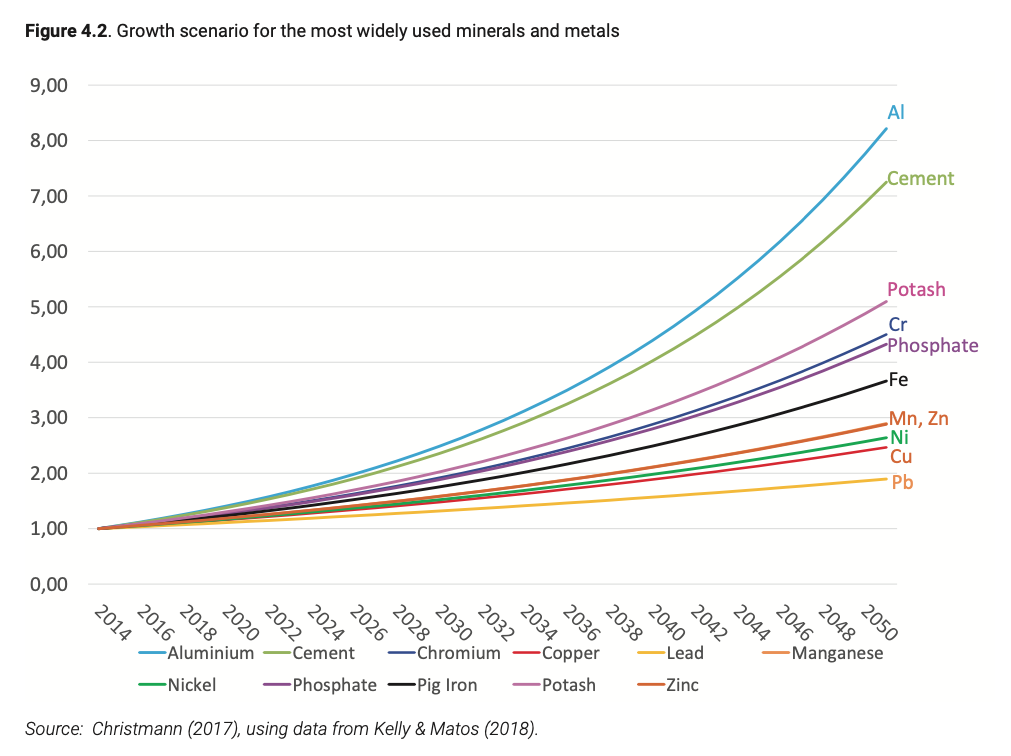

Growth scenario for mineral demand, International Resources Panel 2019

Growth scenario for mineral demand by technology to achieve net-zero scenario - Credits: IEA 2021

Growth scenario for mineral demand by technology to achieve net-zero scenario - Credits: IEA 2021

The energy transition relies on technologies and accelerated electrification that are very metal intensive. The production of batteries and electric vehicles represent a major part of this mineral demand. It seems unlikely that we will have to extract so much mineral at this scale and speed.

We could theoretically continue to push back the limits of known reserves and not experience metal depletion as long as we have an adequate technical knowledge, an attractive resource price, and sufficiently low exploitation costs (and therefore energy costs). Under these conditions, we could go and exploit deposits that are difficult to access, such as non-conventional deposits and deep-sea deposits. However, these conditions will be increasingly difficult to meet, despite an increase in demand, the best deposits have already been exploited and the yields of the deposits are falling. The engineer Philippe Bihouix describes the following vicious circle: ores are less and less concentrated, so more and more energy is needed to extract them, energy equipment uses more and more metals, so it is more and more difficult to produce energy and extract new metals. We can assume that we will have a criticality problem due to an energy problem, a water problem, a social problem and an environmental problem before we have a resource availability problem. It remains to be seen how long we will be able to pay this price and whether we really want to pay this price. Alain Geldron, national expert in raw materials believes that "the depletion of mineral resources before the end of this century is very unlikely for most mineral raw materials, but shortages over a long period of time are to be expected, if new deposits are not exploited quickly enough."

[...] provides arguments for two classically opposed views of the future of mineral resources: an unaffordable increase in costs and prices following the depletion of high quality deposits or, on the contrary, a favourable compensation by technological improvements. Both visions are true, but not at the same time. After a period of gains in energy and production costs, it seems that we are now entering a pivotal period of long-term increasing production costs as we approach the practical minimum energy and thermodynamic limits for several metals. (Vidal et al., 2021)

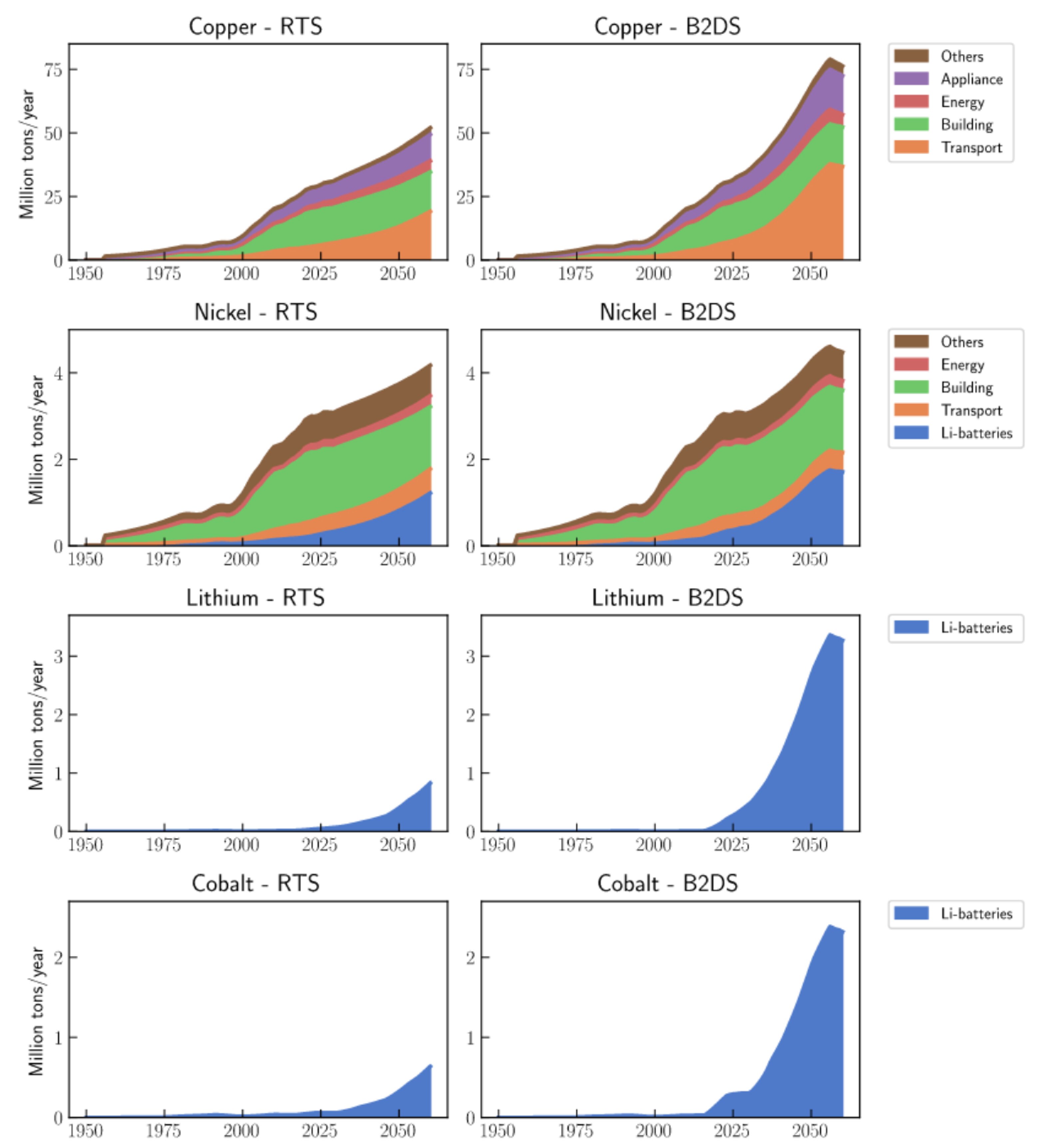

Annual demand for Cu, Li, Ni, and Co calculated for the evolution of infrastructure in the

reference technology (RTS) (Left panel) and the “Beyond 2 ° C” scenario (B2DS) (Right panel) of the

International Energy Agency - Credits: Vidal, 2022

Although these analyses focus on global consumption and production, they conceal the uneven distribution of resources across the planet. The main consumers of raw materials are in the Global North, where the supply of critical materials is increasingly regarded as a strategic issue. Meanwhile, production sites are often located in the Global South, where local populations suffer the social and environmental consequences of extraction.

Activity: Dismantling (40min)

Take apart the device provided by the teacher and try to determine

its composition (metals, plastics, glass...).

You can use the resources below to help you.

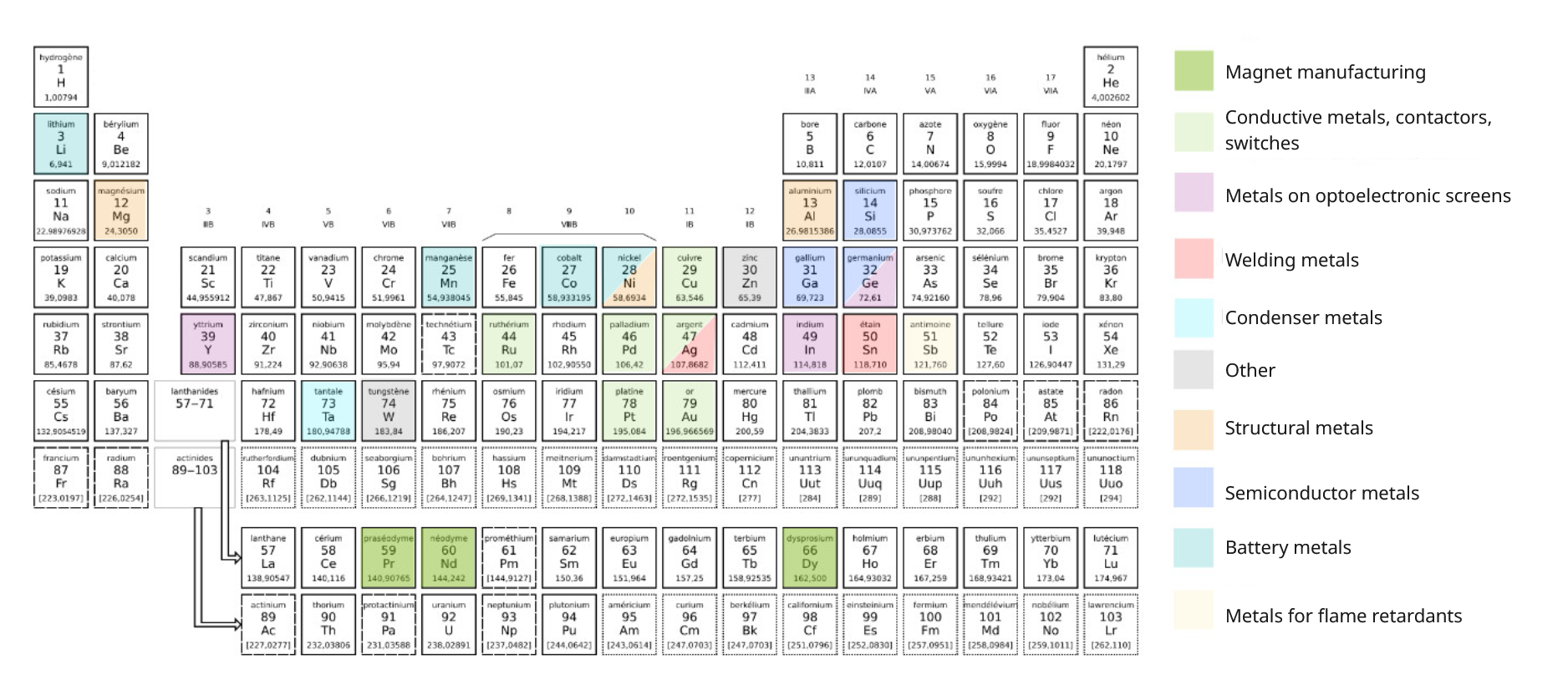

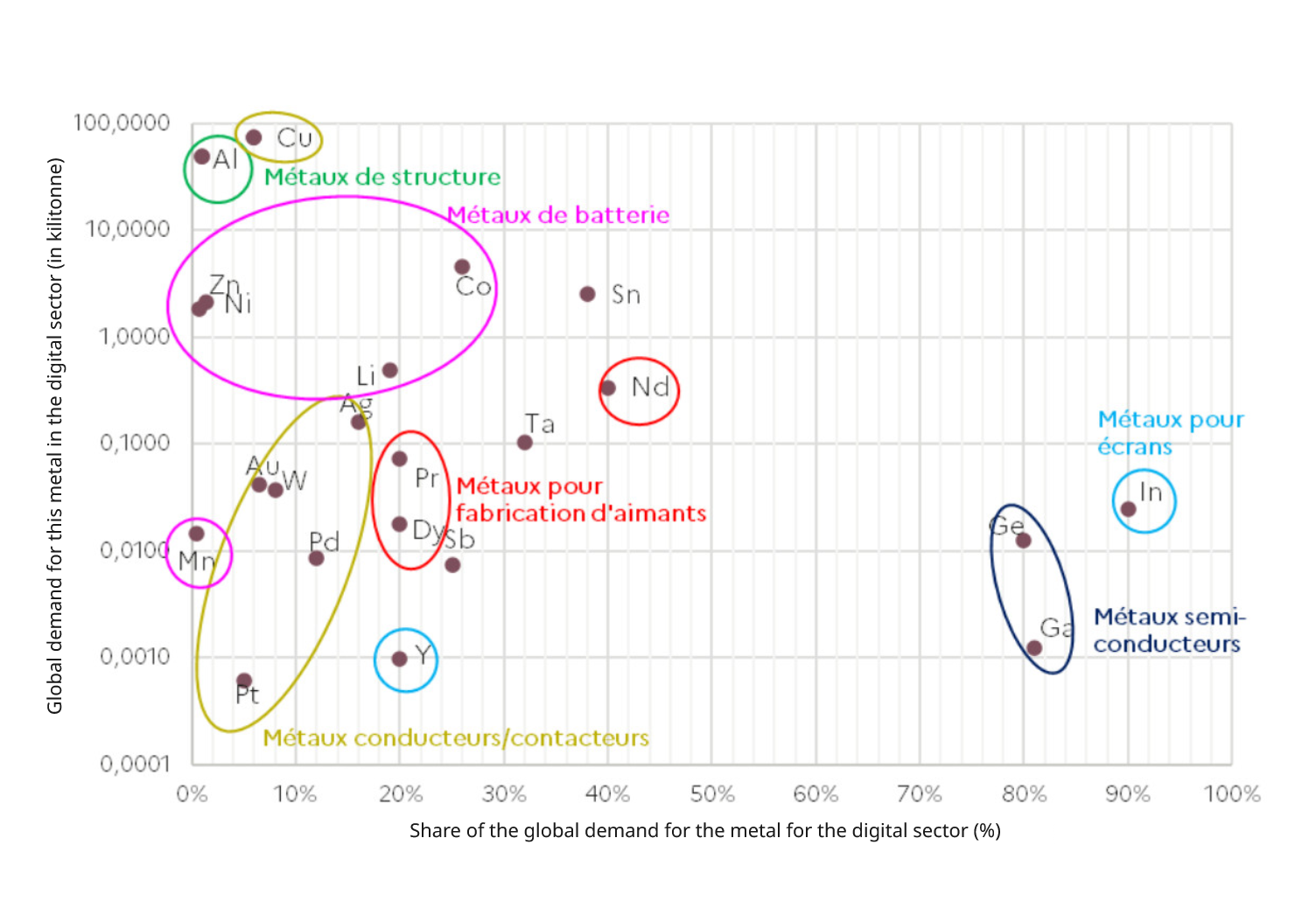

Classification of metals according to their uses in the digital field, ADEME (2024)

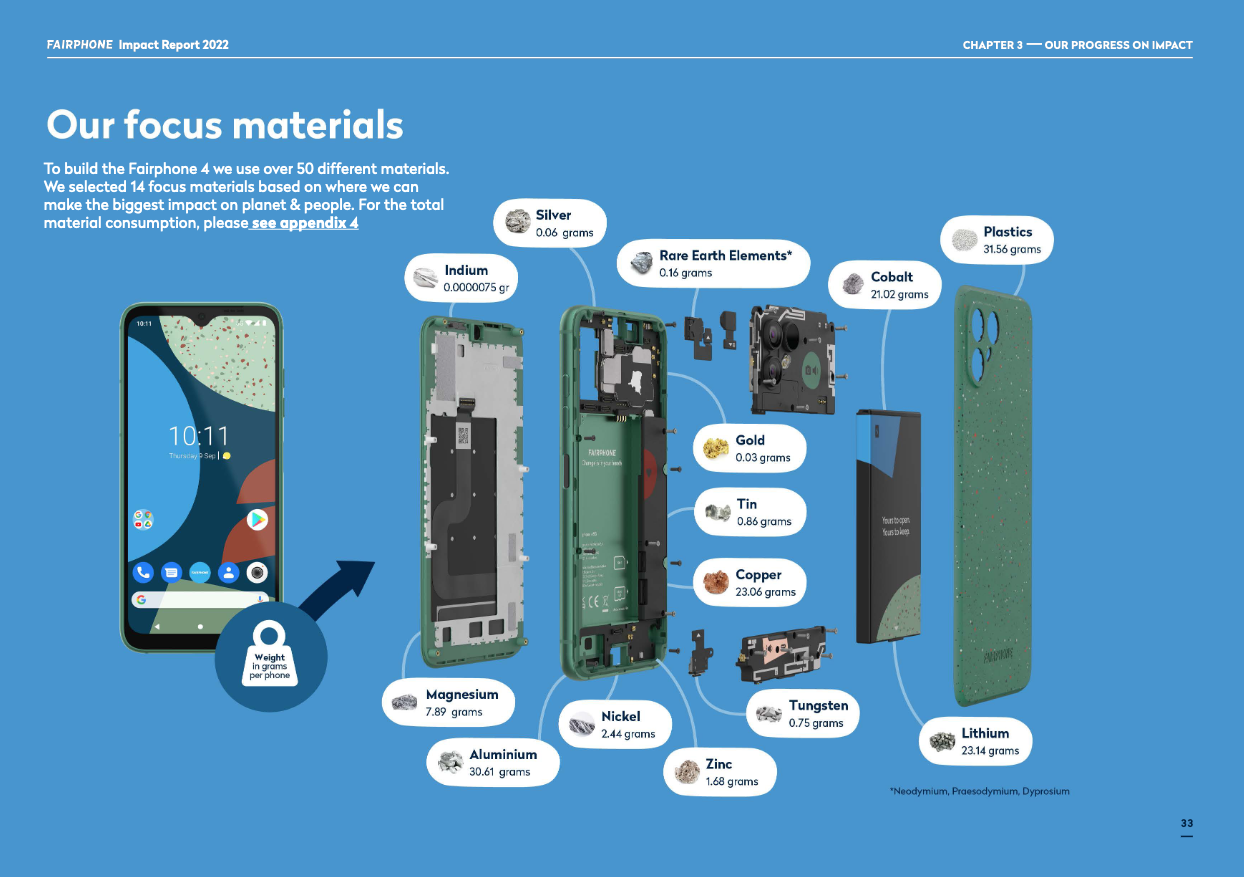

Weight of metals in a Fairphone 4 - Credits: Fairphone

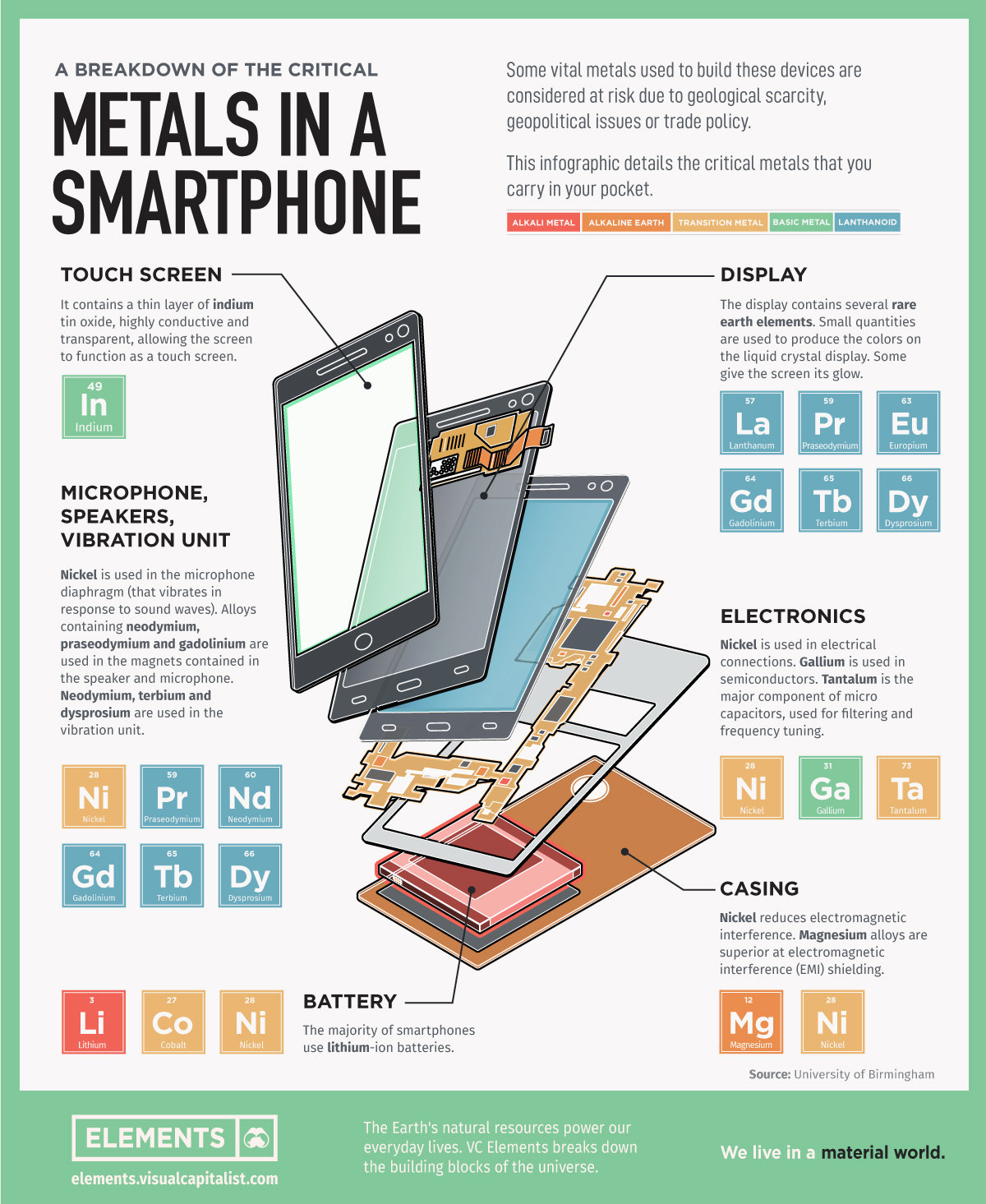

_Visualizing the Critical Metals in a Smartphone - Credits: visual capitalist

Material resources for ICT

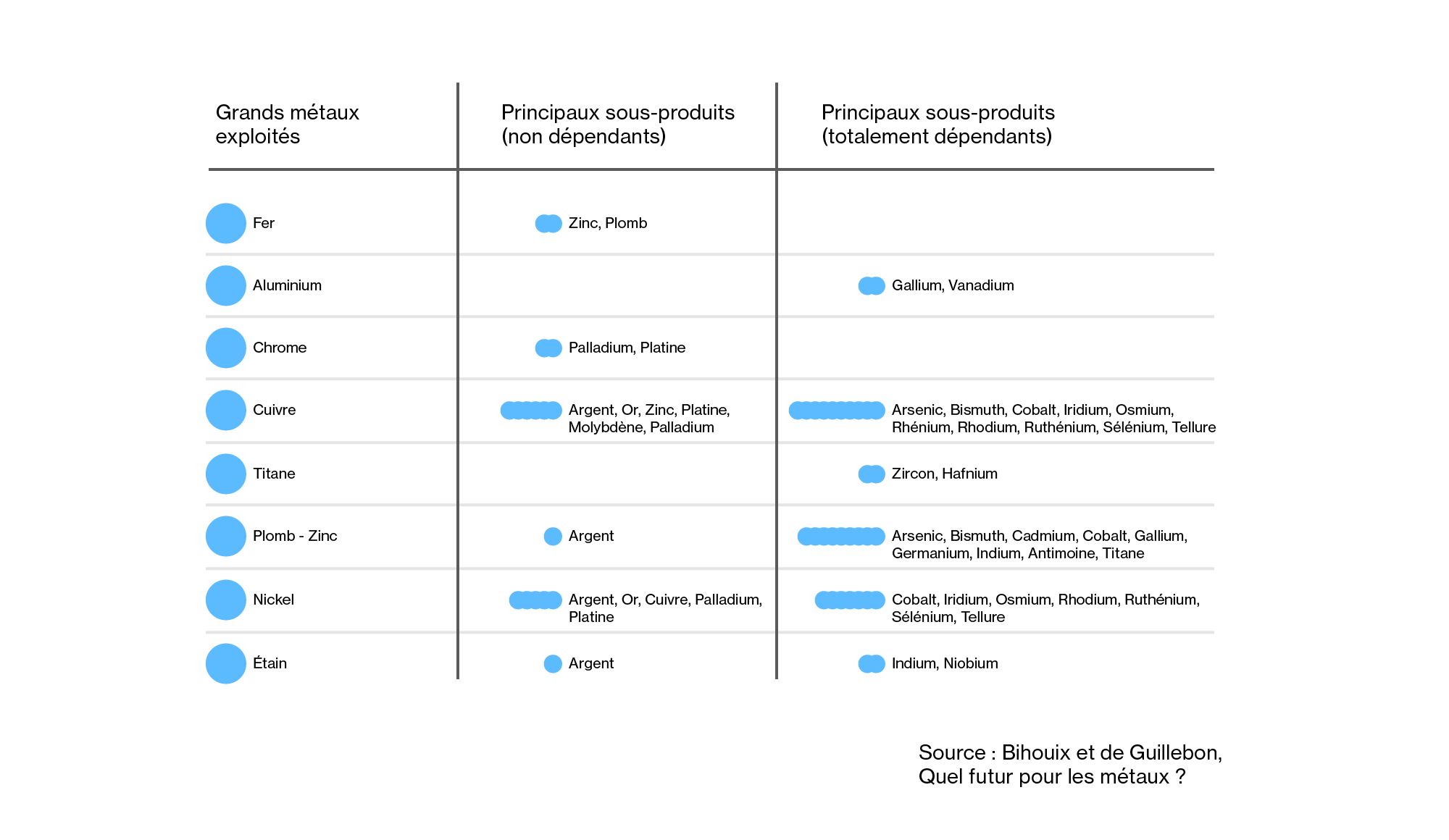

In the digital sector there are two categories of metals, those used in large quantities for their structural functions (telecommunication networks → copper, aluminum, some steels) and metals used in small quantities for their exceptional properties in the high-tech industry (small metals and precious metals). In total, the digital sector solicits more than 60 metals in very diverse volumes and more than half of these metals depend on the extraction of other metals. Indeed, some small metals demanded by the digital sector do not represent a sufficiently large volume of demand to justify the opening of a dedicated mine, so they are extracted in mines whose profitability depends on the massive extraction of large metals. For example, gallium depends on the extraction of aluminum bauxite and germanium is only recoverable from zinc ore. This interdependence can be problematic because it implies that an increase in demand for a small metal will not lead to an increase in supply because it would require an increase in production of the large metal on which the small metal depends. If the demand for germanium increases, then zinc production must be increased, and to justify this increase in production, it must be economically attractive, so the demand for zinc must increase. In short, the supply of small metals and precious metals will not always match the demand because of their co-dependence.

Co-dependence between minerals

So what are the differences in production between large metals and small and precious metals? When it comes to large metals like copper, aluminum, iron or tin for example, their consumption is also increasing. According to the International Copper Study Group, the total consumption of copper in the world amounted to 24 million tons in 2017. The share of consumption related to the use of copper as an electrical conductor reached almost 60%, "that is, about 11 million tons for the generation, distribution and transmission of electricity, and 3 million tons for the subset of electrical and electronic equipment to which digital belongs," as Liliane Dedryver reminds us for France Stratégie. The governemental think tank estimates "that one ton of copper is needed to produce 250,000 smartphones and tablets, the 1.4 billion new smartphones sold worldwide in 2017 (including 20 million in France) required the consumption of 5,600 tons of copper (including 80 tons for France)."

Share of digital technology in user sectors for metals within the scope of the study (Deloitte, based on various data; Malmodin et al., 2018), from ADEME (2024)

On the side of small metals the volumes mined are largely different. For example, the annual production of tantalum was estimated at 1,800 tons in 2017 and 2018. Arround half of the production of this metal was used for the manufacture of electronic capacitors. These capacitors have notably enabled the miniaturization of digital equipment. The manufacture of consumer electronics is driving the majority of the production of this metal and leads to an estimated annual growth rate of 5.8% . Other metals such as gallium and germanium are used for their properties in the manufacture of semiconductors. Their annual production is estimated at 320 and 106 tons respectively. Less than one gram of each of these metals is used in the manufacture of a smartphone. Although the volume produced is small, digital equipment accounts for the bulk of the demand. It is the same for Indium used in touch screens.

Securing critical materiels in Europe

In an effort to increase its sovereignty and strategic autonomy, the European Union recently passed an act aimed at securing its access to critical and strategic metals : European Critical Raw Materials Act. Critical raw materials (CRMs) are defined as raw materials of primary importance to the European economy and are subject to supply chain risks such as dependence, economic risk, scarcity or weak substitutability.

Critical Raw Materials are indispensable for the EU economy and a wide set of necessary technologies for strategic sectors such as renewable energy, digital, aerospace and defence. The Critical Raw Materials Act (CRM Act) will ensure EU access to a secure and sustainable supply of critical raw materials, enabling Europe to meet its 2030 climate and digital objectives.

In a context of increased geopolitical tension and a turn towards protectionism this policy stems from Europe's realisation of its dependencies in particular to China with regard to critical raw materials, many of which are essential for the digital sector, such as gallium, germanium, LREEs or HREEs. It is also driven by an increase in demand from strategic sectors, such as the ecological and digital transitions, as well as increased defence needs.

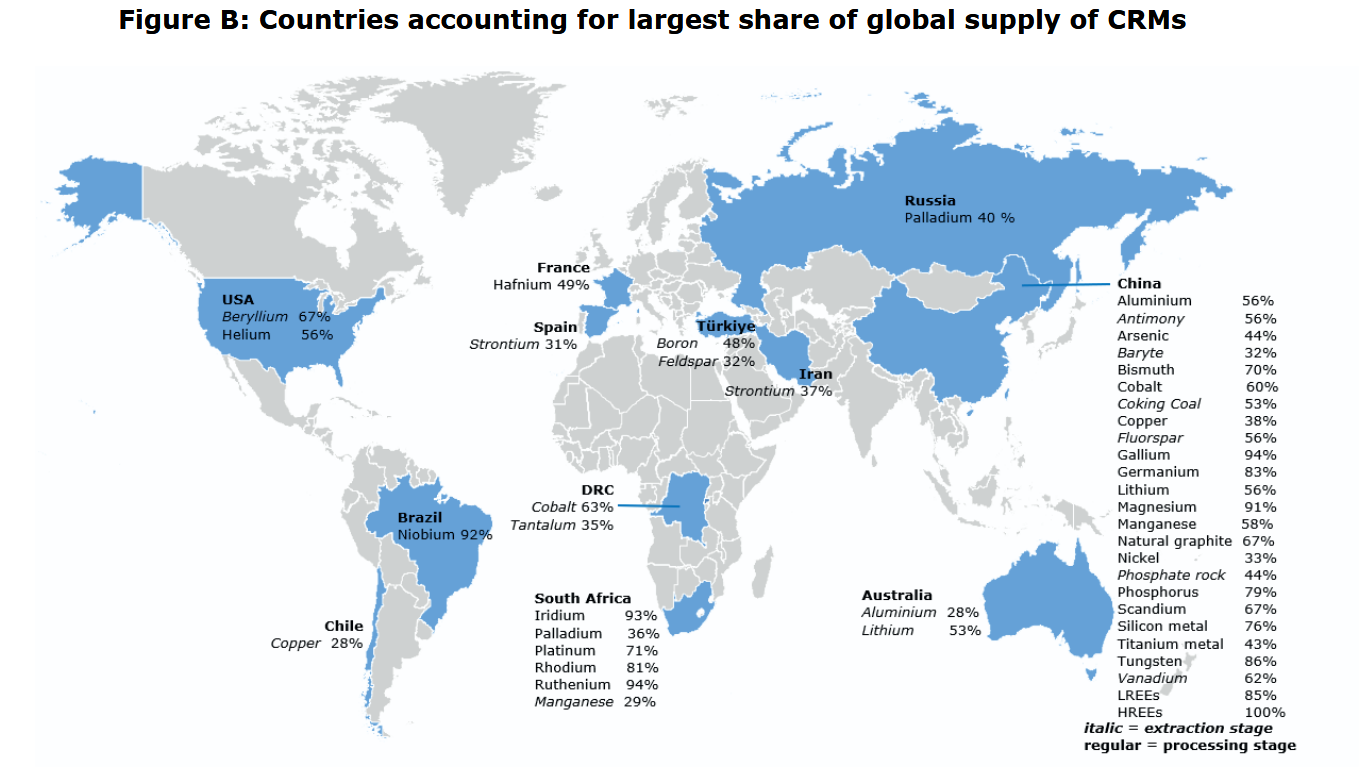

Countries accounting for the largest shart of global supply of CRMs, Study on the review of the list of critical raw materials, Final report, 2017

The EU's Critical Raw Materials Act aims to increase the proportion of metals extracted within the EU to more than 10% of its consumption by 2030, as well as increasing the proportion of processing and recycling within the EU to more than 40% and 25% respectively, while reducing dependence on a single third country to less than 65% of the EU's annual consumption.

Although the Critical Raw Materials Act highlights digital technology, the criticality issues for this sector are, in fact, minor compared to those for other strategic sectors. This is because the quantities used in each device and by the sector as a whole are limited, particularly in the case of the most critical metals. Therefore, an increase in the price of a material would only have a limited effect on the overall price of a devices. Apart from a few specific cases, supply risks in the digital technology sector appear to be more limited than in other strategic sectors.

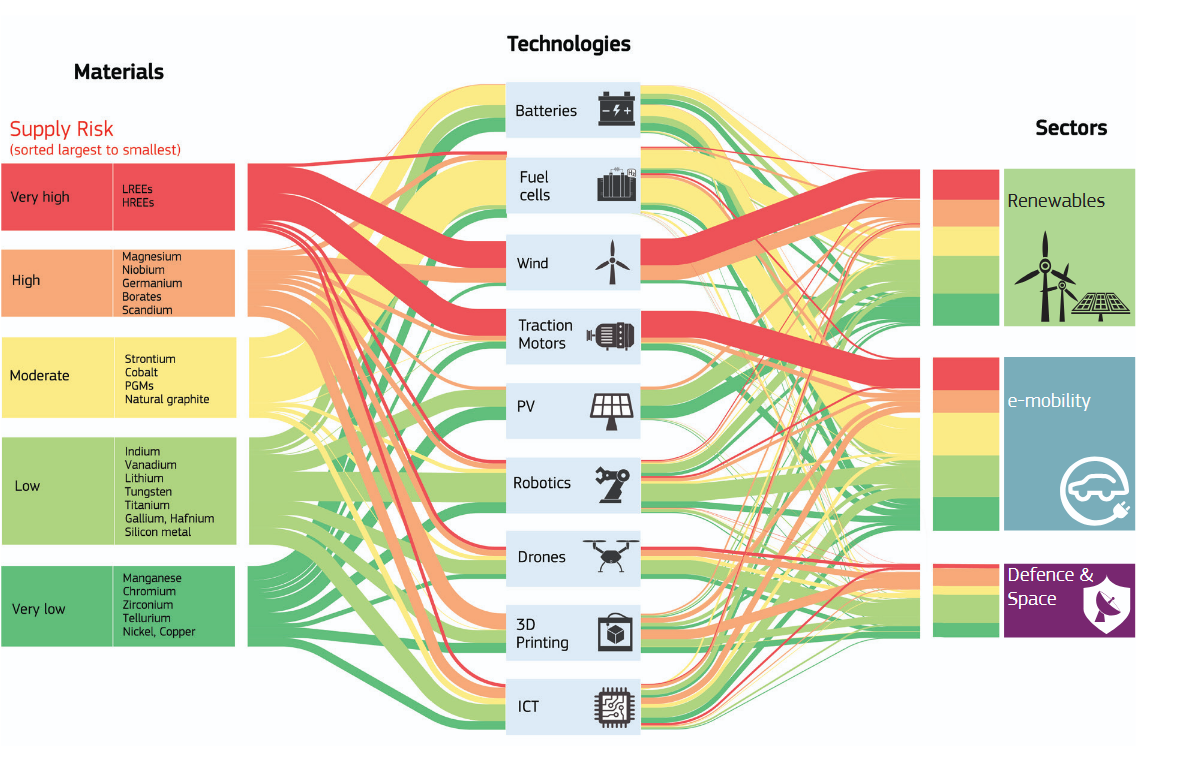

Contribution of different critical materials to technologies and sectors, Critical Raw Materials for Strategic Technologies and Sectors in the EU, JRC, 2020

Social and environmental conflicts

Discovering more deposits and exploiting them is not without consequences. The mining industry is one of the most polluting on Earth due to the use of toxic products, and its massive consumption of energy and water, which also ravages biodiversity and human health. Contrary to what the industry claims, there is no such thing as a clean or green mine. From an environmental point of view, the only thing to do is to limit the number of mines and to make the extraction conditions less dirty.

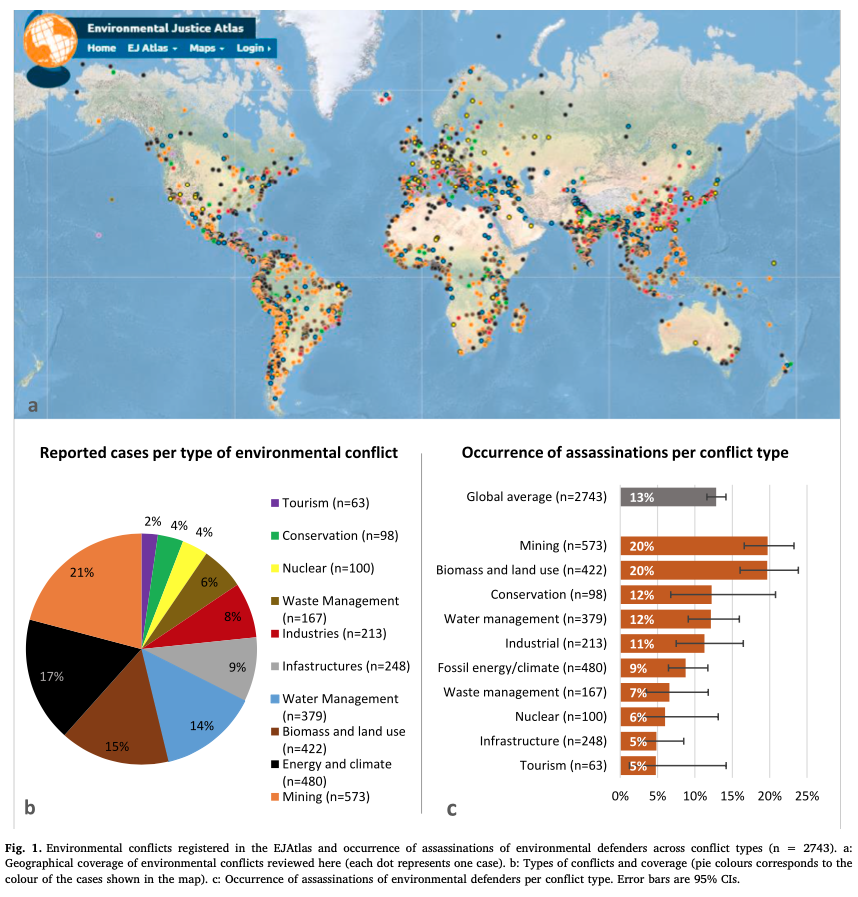

The opening of a mining site is very often a source of conflict. First, there is the issue of land use and land transformation. If the deposit is located in an inhabited area or in an area of high biodiversity, the project is likely to be conflictual. Second, there is the issue of resources needed to operate the mine. For example, large quantities of water are needed for the lithium salars in Chile and create conflicts over water use with local populations. Third, there is the question of pollution linked to the mine: air pollution, water pollution, toxicity for humans, wildlife, voluntary discharges, etc... Thus, the mining sector faces many legitimate challenges from local populations. Unfortunately, this sector has the highest number of killings of environmental activists according to Scheidel et al.

The huge expected increase in mineral resources consumption and primary production will increase conflicts and social opposition. The surface occupied by mines and quarries at the world level has been estimated to be about 400,000 km2 ; it could be doubled by 2050 and quadrupled by 2100. The embodied water consumption and other environmental impacts are expected to follow the same trends. (Vidal et al., 2021)

Environmental conflicts registered in the EJAtlas and occurrence of assassinations of environmental defenders across conflict types - Credits: Scheidel et al. 2020

Moreover, the countries that consume the most mineral resources are generally not those that extract them. This means that pollution, water conflicts and other social and health consequences are not suffered by those who consume the end products. Thus the environmental consequences of the phenomenal increase in mineral demand will be less felt by post-industrial countries. The increase in mineral demand will result in the opening of new mining operations where social unrest may increasingly intensify due to the well known polliutions associated with the mining industry. Potentially, this will reinforce the "need" for more authoritarian regimes to quell local protests in order for mining to expand.

The issue of resources thus goes well beyond environmental issues and brings us directly back to the social, health and political issues related to this sector. A priori, we will not be able to meet the mineral demand envisaged in the future without making the conditions of exploitation more and more unbearable.

The European Commission presents the issue of relocating extraction and processing activities to Europe as both a sovereignty and sustainability issue. Indeed, the environmental standards in Europe could limit certain impacts. However, the mining industry is inherently a source of environmental damage. Furthermore, in a context of rising metal consumption, the relocation of mines would, in reality, be more of an addition than a substitution.

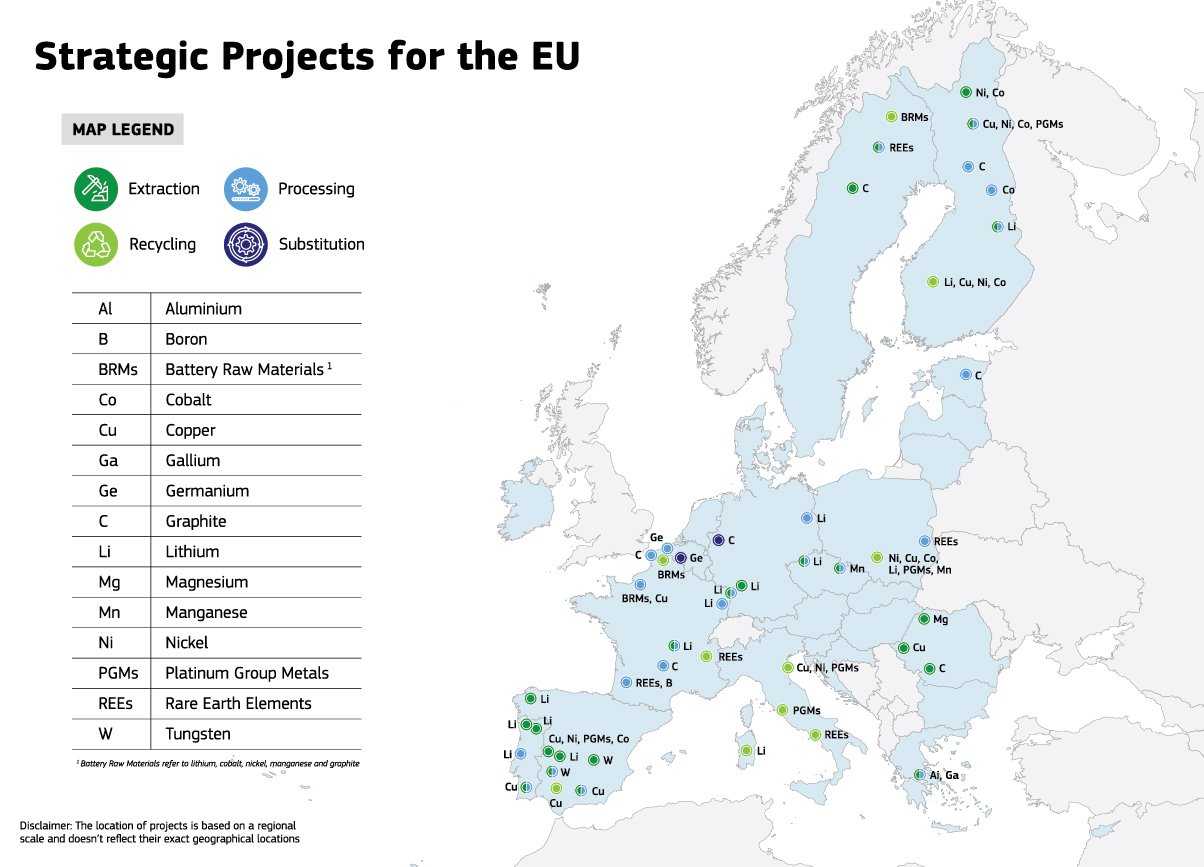

_Strategic Projects for the EU, European Commission. For more informations see the Selected strategic projects.

The limitations of analysing the impacts of digital technology through the lens of mining.

The increase in demand for resources, particularly minerals, compared to the current state of the mining sector indicates that shortages are coming in several metals. If mining projects accelerate then environmental, social and health damage will increase together.

The digital sector does not appear to be the main driver behind the opening of new mines or the sector primarily facing shortages. Most of the metals it relies on are used in small quantities and it is rarely their main consumer. Furthermore, the metals most widely used by digital technologies often are co-depend on other large metals, meaning their supply is not solely determined by the needs of the digital sector. Nevertheless, maintaining the current rate of digital expansion continues to fuel extractivist practices, thereby exacerbating the social and environmental issues associated with mining. Under these conditions, a genuinely clean or fair digital transition is impossible.

In order to understand the main environmental challenges facing the digital sector, it is insufficient to consider them throught the lens of the mining industry alone. To do so, we must look further down the value chain to understand the specific characteristics of the sector in terms of socio-environmental impacts.

Resources

Syllabus

- Dillon Marsh, For What It's Worth, 2018

- Judith Pigneur, The Potential for Responsible Sourcing in the Magnet Value Chain: Strategies for the Future, 2020

- IEA, The Role of Critical Minerals in Clean Energy Transitions, 2021

- Critical Raw Materials for Strategic Technologies and Sectors in the EU, https://rmis.jrc.ec.europa.eu/uploads/CRMs_for_Strategic_Technologies_and_Sectors_in_the_EU_2020.pdf, 2020

To go further

- Olivier Vidal et al., Modelling the Demand and Access of Mineral Resources in a Changing World, 2021

- US Geological Survey, Mineral Commodity Summaries 2023

- Florian Fizaine, The economics of recycling rate: New insights from waste electrical and electronic equipment, 2020

- Liliane Dedryver, La consommation de métaux du numérique : un secteur loin d’être dématérialisé, 2020 [FR]

- Arnim Scheidel et al., Environmental conflicts and defenders: A global overview, 2020

- SystEx, Controverses minières - Pour en finir avec certaines contrevérités sur la mine et les filières minérales - Volet 1, 2021 [FR]